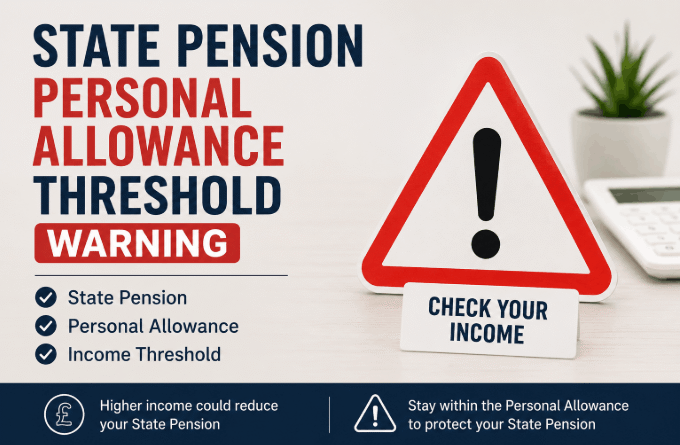

State Pension Personal Allowance Threshold Warning: 2026/27 Tax Freezes And Exemptions

The state pension personal allowance threshold warning refers to the shrinking gap between the full new state pension and the frozen £12,570 income tax threshold, now just £22.40 for the 2026/27 tax year.

Retirees relying solely on the state pension remain protected under a government exemption, but anyone with additional income faces a real risk of an unexpected tax bill, based on figures confirmed as of June 2026.

Key Takeaways

- The full new state pension rose to £12,547.60 a year from 6 April 2026, sitting just £22.40 below the frozen £12,570 personal allowance.

- The personal allowance has been frozen since 2021/22 and is legislated to remain at £12,570 until April 2031 under the Finance No 2 Bill 2024 to 2026.

- Pensioners whose only income is the basic or new state pension, without any increments, are covered by a government exemption, though HMRC confirms the supporting legislation is still pending.

What Does the State Pension Personal Allowance Threshold Warning Mean for Retirees?

The state pension personal allowance threshold warning means many pensioners now sit within a few pounds of paying tax on income they assumed was tax free.

HM Revenue and Customs treats the state pension as taxable income against the same threshold as any other earnings, even though the Department for Work and Pensions pays it without deducting tax.

A private pension, part-time earnings, or savings interest on top of the state pension makes crossing that threshold far more likely.

HMRC usually collects tax owed by adjusting the tax code on a private pension or through a Simple Assessment bill sent directly to the pensioner. Checking a current tax code every year remains the simplest way to catch an error before it turns into a demand for backdated tax.

How Close Is the State Pension to the Personal Allowance in 2026/27?

The full new state pension sits just £22.40 below the personal allowance for the 2026/27 tax year, the narrowest gap since the freeze began.

The state pension rose 4.8% under the triple lock from 6 April 2026, and the Office for Budget Responsibility forecast earlier in 2026 that the increase would land the pension just short of the threshold.

| Tax Year | Full New State Pension Weekly | Full New State Pension Annual | Personal Allowance | Remaining Allowance |

|---|---|---|---|---|

| 2025/26 | £230.25 | £11,973.00 | £12,570 | £597.00 |

| 2026/27 | £241.30 | £12,547.60 | £12,570 | £22.40 |

That leaves barely any room to absorb extra income from a workplace pension or a part time wage before basic rate tax applies.

Why Is the Personal Allowance Frozen Until 2031?

The personal allowance stays at £12,570 because Parliament has legislated the freeze through to April 2031, not April 2028 as some older guidance still states.

This fiscal drag pulls more pensioners into paying tax every year the state pension tax threshold freeze continues, since incomes rise while the threshold itself does not move.

- Finance Act 2021 first fixed the personal allowance at £12,570 from April 2021.

- Finance Act 2023 extended that freeze through the 2027/28 tax year.

- The Finance No 2 Bill 2024 to 2026 extends the freeze again, running to April 2031, according to a House of Commons Library research briefing on the personal allowance.

Anyone still working to an expected 2028 end date should treat April 2031 as the figure that now applies.

Does the State Pension Count Towards the Personal Allowance?

Yes, the state pension counts in full towards the tax free personal allowance, alongside any private pension, employment income, or rental income received in the same tax year. The threshold applies to total income, not to each income stream separately.

Someone drawing the full state pension plus a modest workplace pension has both amounts of pension income added together before HMRC applies the £12,570 threshold. There is no separate allowance reserved for the state pension itself.

HMRC treats the state pension as the first slice of income used against the personal allowance each year.

Anyone receiving £12,547.60 in state pension for 2026/27 has just £22.40 of allowance left for savings interest, a workplace pension, or part time earnings before basic rate tax applies at 20 percent.

What Is the Government State Pension Only Tax Exemption?

Retirees whose sole income is the basic or new state pension will not owe tax on it even if that income alone exceeds the personal allowance, under an exemption announced after the Autumn Budget. Eligibility depends on meeting each of the following conditions.

- The state pension must be the only source of income received in the tax year.

- The exemption covers the basic state pension and the new state pension paid without additional increments such as protected payments.

- Supporting legislation has not yet passed, with HMRC confirming it is expected through a future Finance Bill targeted for April 2027.

Anyone drawing a workplace pension, a part time wage, or rental income alongside the state pension falls outside this exemption and stays liable on income above £12,570.

Why Did Confusion Arise Over the State Pension Tax Exemption?

Confusion arose because the original Autumn Budget wording did not specify who qualified for the exemption, prompting the Low Incomes Tax Reform Group to publicly flag the ambiguity before officials clarified the policy.

LITRG noted the announcement could have been read as covering anyone receiving the state pension, rather than only those with no other income at all.

A named Exchequer Secretary to the Treasury later confirmed in a Commons statement that the exemption applies strictly to pensioners whose only income is the basic or new state pension, without increments.

The House of Commons Library briefing on the personal allowance freeze corroborates the exemption’s narrow scope.

Widely circulated claim: once the state pension exceeds the personal allowance, all pensioners will automatically face a tax bill on it.

Correct position: pensioners whose sole income is the basic or new state pension will not be taxed on it even once it rises above the personal allowance, though anyone with additional income remains liable on the excess.

Source: confirmed via a Commons statement from the Exchequer Secretary to the Treasury, cross-referenced against the House of Commons Library briefing.

How to Avoid Paying Tax on the State Pension?

You can reduce or avoid tax on income sitting near the personal allowance by using a small number of legitimate reliefs before the tax year ends.

- Check your current tax code on the HMRC personal tax account each year to confirm private pension income is taxed correctly.

- Use the Marriage Allowance to transfer up to £1,260 of unused personal allowance to a spouse or civil partner paying basic rate tax.

- Draw additional income from an ISA rather than a taxable pension pot, since ISA income does not count towards the personal allowance.

- Review your private pension drawdown timing to avoid pushing total income just over the threshold in a single tax year.

Do You Pay Tax on the State Pension While Still Working?

Yes, working while receiving the state pension can trigger tax once your combined income passes £12,570, since employment earnings and the state pension are added together. Which scenario applies depends on how that extra income reaches you.

- Employment income taxed through PAYE, with your tax code adjusted to account for the state pension already received.

- Income declared through Self Assessment, with the state pension included as part of total taxable income.

- No employer PAYE income at all, in which case HMRC typically issues a Simple Assessment for any tax owed on the state pension.

More people are staying in work well past state pension age following recent UK state pension age retirement changes, which makes checking a combined tax position worth doing every year. That £12,570 ceiling applies in total, regardless of where the extra income comes from.

How to Verify Your State Pension and Personal Allowance Position?

Confirming an individual position starts with checking a state pension forecast on GOV.UK and a current tax code through HMRC’s personal tax account.

Checking the State Pension Personal Allowance Threshold Warning on GOV.UK

GOV.UK provides a free state pension forecast tool showing the exact annual amount due, along with your qualifying National Insurance contributions and years. Cross check this figure against the current £12,570 personal allowance to see exactly how much headroom remains before other income becomes taxable.

Using HMRC Tax Code Tools

HMRC’s online tax code checker confirms whether a private pension or employment income already accounts for the state pension correctly.

An HMRC state pension tool error occasionally leaves a tax code built on outdated income figures, so it is worth cross checking the result against a P60 or payslip before relying on it.

Conclusion

The state pension personal allowance threshold warning reflects a genuine and narrowing gap, now just £22.40 for the 2026/27 tax year. Retirees with no other income are protected by a pending government exemption, while anyone with additional income should check their tax code through HMRC and GOV.UK.

The state pension personal allowance threshold warning means UK retirees now need to check their own figures each year in 2026/27, rather than assume the old rules still apply.

FAQ

What will happen when State Pension exceeds Personal Allowance?

Pensioners with additional income beyond the state pension will owe basic rate tax on the excess once total income passes £12,570. Those whose only income is the basic or new state pension are covered by a separate government exemption, though HMRC confirms supporting legislation is still pending.

How much income can a pensioner have before paying taxes?

A pensioner can receive up to £12,570 in total income before paying tax, the same personal allowance that applies to any other taxpayer. This figure covers the state pension, private pensions, employment earnings, and most other income combined.

Does the state pension count as taxable income?

Yes, the state pension counts as taxable income, though no tax is deducted at the point of payment. The Department for Work and Pensions pays it gross, and any tax owed is collected later through a tax code adjustment or a Simple Assessment bill.

Do I inherit my husband’s State Pension if he dies?

A surviving spouse may inherit a portion of a late husband’s additional state pension, depending on his National Insurance record and the date he reached state pension age. That qualifying date has moved several times under the UK state pension age increase, so his exact age at the time is worth confirming before assuming the standard inheritance rate applies.

How much savings can a state pensioner have in the bank in the UK?

There is no savings limit that affects state pension eligibility, since it is not means tested. Interest earned on savings does count towards the personal allowance and the personal savings allowance, so a large savings balance can still contribute to a tax bill.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice; please consult a qualified professional regarding your specific tax situation.