UK State Pension Age Increase 2026 To 67: Birth Year Timetable And National Insurance Guide

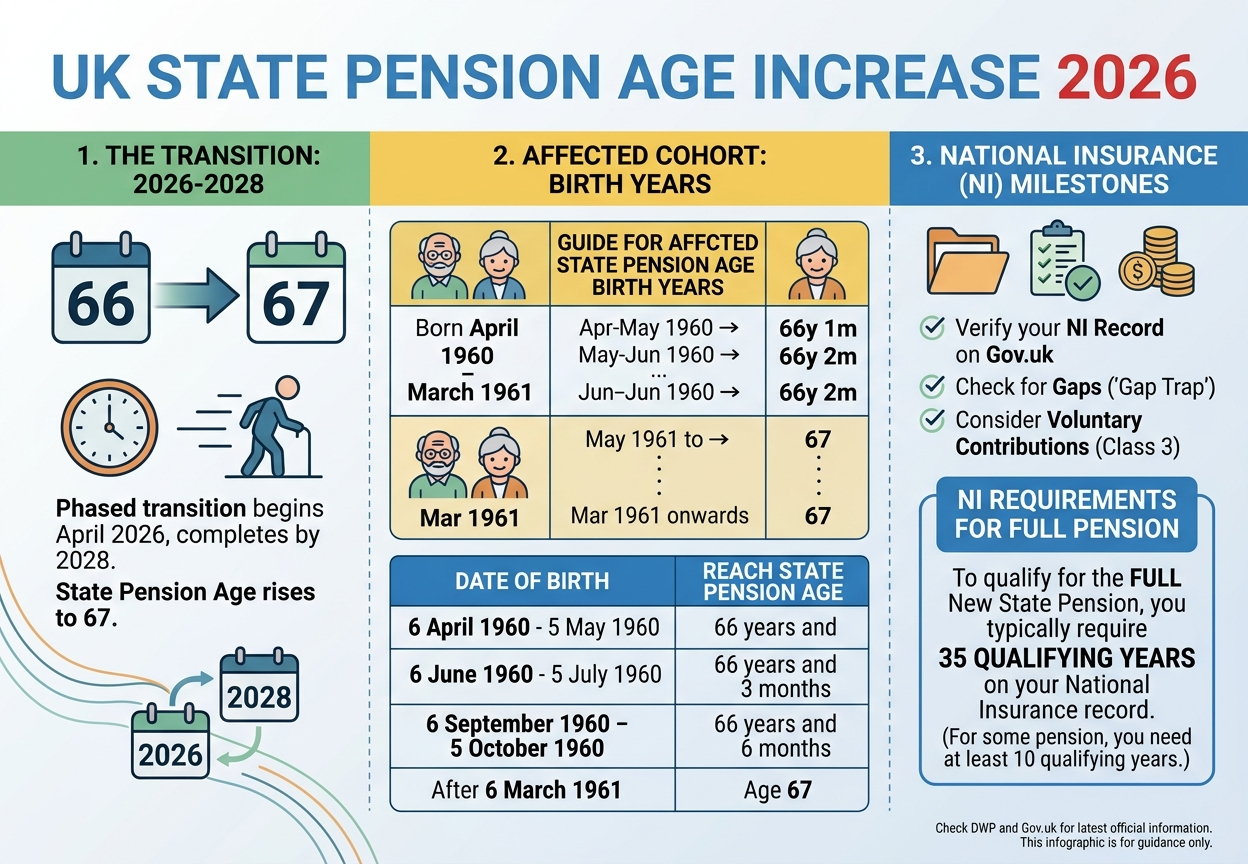

The UK state pension age increase from 66 to 67 will begin a phased rollout in April 2026, fully concluding by 2028. This legislative shift, mandated by the Pensions Act 2014, affects anyone born between April 1960 and March 1961, effectively extending the required working life before state benefit eligibility.

While the move to age 67 has been planned for a decade, the transition creates specific complexities for those nearing retirement. It is not an overnight change but a structured increase that requires a precise understanding of birth dates and National Insurance (NI) milestones.

Key Takeaways

- Transition Period: The shift from age 66 to 67 occurs between 6 April 2026 and 5 April 2028.

- Affected Cohort: Individuals born between 6 April 1960 and 5 April 1977 will have a State Pension age of at least 67.

- Legislative Authority: These changes are governed by the Department for Work and Pensions (DWP) under the Pensions Act 2014.

- Future Outlook: A further increase to age 68 is currently scheduled for between 2044 and 2046, though this is subject to ongoing government review.

Grasping these specific dates is essential for a smooth transition into retirement. Staying informed on the DWP state pension age change 2026 ensures you aren’t caught off guard by the shifting legislative timeline. Staying ahead of these shifts is vital for anyone born in the early 1960s to avoid financial surprises.

Key Fact: To qualify for the full New State Pension in 2026/27, you typically need 35 qualifying years on your National Insurance record. If you have fewer than 10 qualifying years, you may not be entitled to any State Pension payment at all.

UK state pension age increase birth year guide for 2026

The UK state pension age increase in 2026 for specific birth years follows a graduated timetable to avoid a cliff-edge scenario where neighbors born days apart face years of difference in retirement dates.

According to DWP guidelines, if you were born between 6 April 1960 and 5 May 1960, your State Pension age will be 66 years and 1 month. This incremental staircase continues until those born after 6 March 1961 reach the flat age requirement of 67.

Is Your Retirement Date Moving?

The UK state pension age increase to 67 from 2026 for specific birth years is a response to increasing life expectancy and the fiscal sustainability of the Triple Lock system. By raising the age, the Treasury aims to balance the ratio of workers to retirees.

For you to qualify for any State Pension, you generally need 10 qualifying years on your National Insurance record.

To receive the full new State Pension, you typically require 35 qualifying years. You should verify your NI record via the Government Gateway to ensure no gaps exist that could further delay your financial security.

Many people often ask How much State Pension will I get at 66 if they reach eligibility just before the transition begins. Knowing your projected amount helps in calculating the bridge funding required for a later retirement date.

Avoid National Insurance gaps during the UK state pension age increase

A technical detail often overlooked is the NI Gap Trap, which can affect your final payout. While a later pension age offers more time to contribute, it also creates a longer income shortfall to cover if you stop work at 66.

If you plan to retire at 66 but cannot claim your State Pension until 67, you may face a 12-month income gap.

You must ensure you don’t inadvertently trigger a break in your NI record during this final year, as this could impact your final payment amount. Check your record for voluntary contributions (Class 3) to bridge these gaps.

Fact-checking myths about the UK state pension age increase

It is worth separating the headlines from actual DWP policy to ensure your retirement plans are based on facts. The table below breaks down exactly what the current law says versus common retirement myths.

| Myth | Regulatory Reality |

| The increase to 67 was cancelled in 2025. | False. The increase remains law under the Pensions Act 2014 and starts in April 2026. |

| You can claim State Pension early at a reduced rate. | False. Unlike some private pensions, the UK State Pension cannot be claimed before your official retirement age. |

| 2026 is when the age rises to 68. | False. 2026 marks the start of the rise to 67. The rise to 68 is scheduled for the mid-2040s. |

| Everyone born in 1960 retires at 67. | False. It depends on the month. Those born early in the tax year (April/May) retire at 66 and a few months. |

| You stop paying NI as soon as you hit 66. | False. You pay NI until you reach your actual State Pension age, even if that is 67. |

Will the State Pension Age Increase to 70?

There is currently no legislation in place to raise the State Pension age to 70. While think tanks and the Office for Budget Responsibility (OBR) often discuss the fiscal necessity of higher ages, the current legal trajectory stops at 68.

Any move to age 70 would require a new Act of Parliament and a significant period of public consultation. Historically, the government provides at least 10 years’ notice before such a substantial change is implemented.

Can I Retire at 62 and Get State Pension in the UK?

You cannot receive your UK State Pension at age 62. The earliest you can currently access this benefit is your 66th birthday (rising to 67 in 2026). However, you can choose to retire from work at 62 if you have sufficient private savings, workplace pensions, or investments to sustain you until your State Pension age is reached.

You can retire whenever you choose, but the State Pension remains locked until your official age. If you retire at 62, you must fund your lifestyle independently for several years.

Does a Woman Who Has Never Worked Get a State Pension?

A woman who has never been in paid employment may still qualify for a State Pension through National Insurance credits. These are often applied automatically for those who were raising children (Child Benefit), acting as a carer, or receiving certain disability benefits.

If you reached State Pension age before 6 April 2016, you might have been able to claim a pension based on your husband’s NI record.

Under the new State Pension system, eligibility is strictly based on your own record or inherited credits in very specific circumstances.

This shift has led to ongoing debates regarding the new state pension being unfair to existing pensioners who reached retirement age under the old rules. These disparities highlight why personal NI audits are so critical today.

Find your retirement date with the UK state pension age increase chart

Because the transition to age 67 is phased, your exact qualifying date depends entirely on your month of birth. Use the timetable below to identify exactly when you will reach eligibility under the new UK state pension age increase schedule.

| Date of Birth | Date State Pension Age Reached |

| 6 April 1960 – 5 May 1960 | 66 years and 1 month |

| 6 May 1960 – 5 June 1960 | 66 years and 2 months |

| 6 June 1960 – 5 July 1960 | 66 years and 3 months |

| 6 July 1960 – 5 August 1960 | 66 years and 4 months |

| 6 August 1960 – 5 September 1960 | 66 years and 5 months |

| 6 September 1960 – 5 October 1960 | 66 years and 6 months |

Future impact of the UK state pension age increase to 68

Following the 2026–2028 transition, the next milestone is the state pension age increase to 68. Current law places this increase between 2044 and 2046. However, the Cridland Review suggested this should be brought forward to 2037–2039.

The government has deferred the decision on accelerating the rise to 68 until a further review is conducted, likely in 2027 or 2028. This uncertainty surrounding long-term UK state pension age retirement changes means for anyone born in the 1970s or later, the age 68 target remains a moving legislative target.

How to Check Your Specific State Pension Forecast?

To ensure your retirement planning is accurate, follow these essential steps to access your personalized forecast and identify any potential gaps in your record:

- Visit the official Check your State Pension service on GOV.UK.

- Log in using your Government Gateway ID or GOV.UK One Login.

- View your projected weekly, monthly, and yearly payment amounts.

- Identify the exact date you will reach State Pension age.

- Review your National Insurance record for full or partial years.

- Check for any Gaps and calculate the cost of buying voluntary years if necessary.

Conclusion

Planning for the UK state pension age increase means looking past the headlines and checking your specific birth month. The shift to 67 is a firm legislative reality that demands a proactive audit of your National Insurance record and private retirement provisions.

By understanding the phased transition starting in 2026, you can bridge potential income gaps and ensure your transition into retirement is financially stable.

Some news outlets have reported that the age 67 increase was under review for cancellation. This is incorrect. While the timing of the increase to 68 was deferred, the increase to 67 starting in 2026 is legally settled under the Pensions Act 2014 and is currently being implemented by the DWP.

FAQ

Is there a state pension age increase 2026 latest news update?

Yes. As of May 2026, the DWP has confirmed that the transition to age 67 is proceeding as scheduled. There have been no legislative amendments to pause or cancel the shift. Taxpayers are encouraged to check their personal forecasts to see their specific retirement date.

Is the state pension age 66 or 67 right now?

Yes and no. Currently, the State Pension age is 66 for both men and women. However, for those turning 66 after April 2026, the age begins to climb incrementally toward 67. By 2028, the age will be 67 for everyone.

What is considered a rich pensioner in the UK?

There is no official DWP definition of a rich pensioner. However, the ONS often categorizes the top 10% of retiree households as those with a total income (including private pensions and investments) exceeding £45,000 per year after tax.

Do I get my husband’s State Pension when he dies?

This depends on when you both reached State Pension age. Under the new State Pension system, you may be able to inherit a portion of your partner’s protected payment or extra State Pension if your marriage or civil partnership began before 6 April 2016.

How much savings can a state pensioner have in the bank in the UK?

There is no limit to how much savings you can have to receive the State Pension. It is a non-means-tested benefit based on NI contributions. However, if you claim Pension Credit, savings over £10,000 will affect your eligibility.

Will the State Pension increase in 2026?

Yes. Under the Triple Lock mechanism, the State Pension increases every April by the highest of inflation, average earnings growth, or 2.5%. The exact 2026/27 rates are usually confirmed in the preceding Autumn Statement.

Is 1200 a month pension good in the UK?

A monthly income of £1,200 (£14,400 per year) is slightly above the full New State Pension but below the Minimum Living Standard for a single retiree as defined by the Pensions and Lifetime Savings Association (PLSA), which currently sits around £14,400 to £15,000.

How much is the State Pension increasing in April 2026?

Yes, the State Pension is set for a significant boost. Under the Triple Lock guarantee, the full New State Pension will rise by 4.8% in April 2026, increasing from £230.25 to £241.30 per week (£12,547.60 per year).

Can I increase my payment by deferring my State Pension in 2026?

Yes. If you do not claim your State Pension immediately upon reaching your new qualifying age, your weekly payment will increase by approximately 5.8% for every full year you defer. You must defer for at least nine weeks to see an increase in your payments.

Will I be notified by the DWP before my pension age changes?

Yes. The Pension Service typically sends an invitation to claim your State Pension approximately four months before you reach your official State Pension age. It is vital to ensure your contact details are up to date with HMRC to receive this notification on time.

Disclaimer: This article provides general information on the UK state pension age increase for educational purposes only and does not constitute official financial or legal advice; please consult the DWP or a qualified financial advisor for your specific circumstances.