Defined Contribution vs Defined Benefit Pension Plan: Guaranteed Income, Transfer Rules, Investment Risk and the 2027 IHT Changes Explained

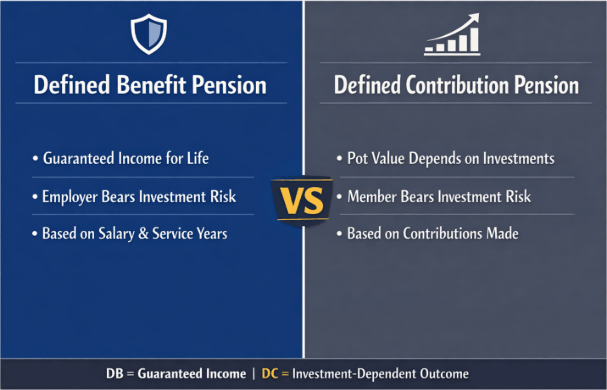

A defined benefit pension guarantees a fixed annual income in retirement, calculated from salary and length of service and overseen by The Pensions Regulator, investment performance plays no role. A defined contribution pension builds a pot of money from employer and employee contributions invested in financial markets; the final value is not guaranteed, and the saver bears all investment risk.

In financial terms, the gap between them is straightforward: one pays a guaranteed income, the other does not.

Key Takeaways

- A defined benefit pension pays a guaranteed income for life based on salary and service length; a defined contribution pension provides a pot whose value depends entirely on investment returns and contributions made.

- Under the Pension Schemes Act 2015, any defined benefit pension transfer worth more than £30,000 requires independent financial advice from an FCA-authorised adviser before it can legally proceed.

- The Pension Protection Fund compensates DB members if their employer becomes insolvent, but compensation is capped at £44,237.62 per year at age 65 (2024/25) and applies at 90% for members who have not yet reached normal pension age.

- Under the Pension Schemes Bill 2025, DC pension pots are set to fall within the scope of Inheritance Tax from April 2027, with direct consequences for estate planning decisions made before that date.

What Is a Defined Benefit Pension and How Does It Work?

A defined benefit pension pays a guaranteed income for life in retirement, determined by salary and length of service, not by contributions made or how scheme investments perform. The employer funds the scheme and covers any shortfall, bearing the investment risk entirely.

Defined benefit schemes fall into two structures, and the difference between them directly affects what a member receives at retirement.

A Career Average Revalued Earnings (CARE) scheme uses average salary across the full membership period, with each year’s earnings revalued annually.

The NHS Pension Scheme and the Local Government Pension Scheme (LGPS) both operate on a CARE basis following the 2015 public sector reforms.

How the Accrual Rate Shapes the Pension You Receive?

Retirement income is calculated using an accrual rate, a fraction set by the scheme rules, determining how much pension is earned per year of service. Common UK rates are 1/60th and 1/80th.

Worked example: A member with 25 years of service in a final salary scheme, earning £36,000 at retirement, on a 1/60th accrual rate, receives an annual pension of £15,000. The same calculation on a 1/80th rate produces £11,250, a £3,750 annual difference for life, illustrating why the accrual rate is the most important figure in any DB pension comparison.

What Is a Defined Contribution Pension and How Does It Work?

A defined contribution pension builds a retirement pot from employer and employee contributions invested in financial markets, but provides no income guarantee. Under the Pensions Act 2008, employers must auto-enrol eligible workers, with minimum contributions of 3% from the employer and 5% from the employee, including tax relief for 2025/26.

DC pensions take several forms, group personal pensions, master trust schemes such as NEST, self-invested personal pensions (SIPPs), and stakeholder pensions, each operating under the same contribution and investment framework.

Tax relief makes DC pensions cost-efficient to build, HMRC applies relief at the member’s marginal income tax rate, reducing the effective cost of each pound contributed throughout the working years.

Your Options When the DC Pension Matures

At retirement, members can take up to 25% of the pot as a tax-free lump sum, subject to the Lump Sum Allowance of £268,275, which replaced the abolished Lifetime Allowance in April 2024.

The remainder can be accessed through income drawdown, converted to an annuity, or withdrawn as lump sums, none of which a defined benefit scheme permits.

Defined Contribution and Defined Benefit Pensions: Myth vs Reality

| Myth | Reality |

|---|---|

| DB pensions are always the better option | DB offers superior income security; DC offers greater portability and flexibility. Neither is universally superior, individual circumstances determine the stronger choice. |

| PPF protection means a full DB pension is guaranteed | PPF compensation is capped at £44,237.62 per year at age 65 (2024/25) and applies at 90% for pre-retirement-age members. Higher earners may receive significantly less than promised. |

| DC pension money is fully safe because it belongs to the member | DC pots are subject to investment risk. FSCS protection covers up to £85,000 per authorised provider, not an unlimited guarantee. |

| Any DB pension can be freely transferred to DC | Transfers above £30,000 require FCA-regulated mandatory advice. Several public sector schemes, including the NHS and Teachers’ Pension Schemes, prohibit transfers entirely. |

| The Lifetime Allowance still restricts pension savings | The Lifetime Allowance was abolished in April 2024. The Lump Sum Allowance of £268,275 now governs the maximum tax-free cash available at retirement. |

| Final salary and defined benefit mean the same thing | Defined benefit includes both final salary and CARE schemes, these structures calculate benefits differently and can produce materially different retirement incomes for the same member. |

| Only public sector workers have access to DB pensions | Some private sector DB schemes remain open to accrual, though the number is declining sharply as employers replace them with DC arrangements for new entrants. |

Which Is Better: A Defined Benefit or Defined Contribution Pension?

For guaranteed income security and inflation protection, a defined benefit pension is the stronger arrangement. For flexibility, portability, and estate planning, a defined contribution pension offers advantages no DB scheme can replicate. The right answer depends entirely on individual circumstances.

The sharpest difference between the two schemes is who absorbs the cost of poor investment returns.

In a DB scheme, the employer absorbs market underperformance entirely, the member’s income is insulated from every downturn the scheme’s assets encounter. In a DC scheme, those same market movements land directly in the member’s pot, with no backstop and no employer covering the gap.

When DB Is Worth Preserving and When DC Makes More Sense?

Career changers and those who move between employers frequently tend to build stronger retirement outcomes through DC, where portability gives them an advantage no DB scheme can replicate.

Those with long service in a single employer or sector, particularly in the public sector, will almost always benefit from preserving DB accrual rather than seeking DC flexibility.

For most private sector workers, DC is the only available option in practice. For anyone with access to an active employer DB scheme, preserving it is almost always the stronger financial decision.

A substantial guaranteed DB income also carries wider retirement implications, it can affect eligibility for means-tested state support, including the winter fuel payment clawback 2026, which now applies only to those on qualifying benefits such as Pension Credit.

DB vs DC Death Benefits: What Happens to Your Pension When You Die?

DB and DC pensions operate under entirely different death benefit rules, and for members with estate planning goals, the distinction carries more weight now than at any point in the past decade.

DB schemes are restricted to providing a taxable income for qualifying dependants on the member’s death. There is no mechanism to pass a DB pension as a lump sum to adult children or other non-dependant beneficiaries, regardless of the scheme’s accumulated value.

DC pensions are built differently. The member nominates beneficiaries, including adult children and other relatives, and the pot can be paid as a lump sum, used to provide a drawdown income, or converted to an annuity.

Where the member dies before age 75, DC death benefits are generally free of income tax for the recipient, and DC pension pots currently sit outside the taxable estate for Inheritance Tax purposes entirely.

Why the April 2027 IHT Change Makes the DC Death Benefit Advantage Time-Limited?

That changes from April 2027. Under the Pension Schemes Bill 2025, unused DC pension savings will be brought within the IHT estate. DC holders with estate planning objectives need to act before that date, there is a specific window available now that closes permanently when the rules change.

The question of how to avoid Inheritance Tax on pensions carries immediate practical weight for anyone in that position.

When a defined contribution pension member dies before age 75, death benefits are currently paid free of income tax to nominated beneficiaries and sit outside the Inheritance Tax estate entirely.

A defined benefit pension can only provide a taxable income to qualifying dependants, no lump sum can be passed to non-dependant beneficiaries, regardless of the scheme’s size or the member’s wishes.

What Happens to a Defined Benefit Pension If an Employer Goes Bust?

When a DB scheme employer becomes insolvent, the Pension Protection Fund steps in, but that protection is not unconditional, and higher-earning members may receive materially less than the pension originally promised.

The PPF pays 100% of the promised pension to members who have already reached the scheme’s normal pension age at insolvency. Members who have not yet reached normal pension age receive 90% of the promised pension, subject to a compensation cap.

According to the Pension Protection Fund, the compensation cap for 2024/25 stands at £44,237.62 per year at age 65, adjusted downward for each year below that age at the point of insolvency.

What the PPF Compensation Cap Means in Practice?

Key Fact: A DB scheme member promised £70,000 per year who had not yet reached normal pension age when their employer became insolvent would receive PPF compensation of approximately £39,813, less than 57 pence for every pound of pension promised.

The cap reflects the PPF’s nature as a levy-funded lifeboat scheme with finite resources, not a full government guarantee.

DC pension pots held with FCA-authorised providers are covered by the Financial Services Compensation Scheme (FSCS) up to £85,000 per authorised provider, providing a separate and distinct protection mechanism.

It is widely assumed that PPF protection guarantees a DB member their full promised income if an employer fails. That is not the case.

PPF compensation is capped at £44,237.62 per year at age 65 (2024/25) and applies at 90% for members below normal pension age, meaning higher earners may receive significantly less than promised. Source: Pension Protection Fund, Compensation Limits 2024/25.

Defined Contribution vs Defined Benefit Pension Plan: Key Features at a Glance

| Feature | Defined Benefit | Defined Contribution |

|---|---|---|

| Retirement income | Guaranteed fixed income for life | Variable, depends on pot value and access method |

| Investment risk | Borne entirely by the employer | Borne entirely by the members |

| Employer role | Funds scheme; covers shortfall | Minimum 3% contribution of qualifying earnings (Pensions Act 2008) |

| Investment decisions | Made by scheme trustees | Made by a member or a default fund |

| Death benefits | Dependant’s income only, taxed | Flexible beneficiaries; tax-free before age 75 |

| Insolvency protection | PPF, capped; 90% rule applies | FSCS, up to £85,000 per FCA-authorised provider |

| Transfer rules | FCA mandatory advice above £30,000; some schemes prohibit transfers | Generally portable; no mandatory advice required |

| Pension Freedoms access | No | Yes, drawdown, annuity, or lump sum |

| Typical sector | Public sector; legacy private sector | Private sector; most new workplace schemes |

Can I Transfer a Defined Benefit Pension to a Defined Contribution Scheme?

Transferring a DB pension to a DC scheme is possible in most cases, but for any transfer value above £30,000, independent financial advice from an FCA-authorised pension transfer specialist is a legal requirement under section 48 of the Pension Schemes Act 2015.

The transfer value, the Cash Equivalent Transfer Value (CETV), is the capital sum the DB scheme pays to a DC arrangement in exchange for surrendering all rights to the guaranteed income.

Giving up safeguarded benefits means accepting full investment risk and relinquishing an inflation-linked income for life. The FCA’s position is that the majority of DB-to-DC transfers are not in the member’s best financial interest.

Which DB Schemes Cannot Be Transferred?

Six named scheme categories sit outside the transfer rules entirely, members of the NHS Pension Scheme, the Teachers’ Pension Scheme, the Civil Service Pension Scheme, and the Police, Armed Forces, and Fire Brigade schemes cannot transfer to a DC arrangement under any circumstances.

The Transfer Process: Four Steps

- Request a formal CETV quotation from the DB scheme administrator, the figure is guaranteed for three months from the date of issue.

- Confirm whether the scheme permits transfers, members of those named public sector schemes cannot proceed regardless of the transfer value.

- Where the transfer value exceeds £30,000, instruct an FCA-authorised pension transfer specialist for the mandatory advice assessment before submitting any transfer instruction.

- If proceeding, instruct the transfer in writing to both the DB scheme and the receiving DC provider, the decision is irreversible once completed.

For anyone unsure whether their scheme permits a transfer or where to find an FCA-regulated specialist, MoneyHelper’s pension guidance service covers both and is free to access.

The Risks of a Defined Contribution Pension: What DC Savers Need to Know?

DC pension holders face three distinct risks that defined benefit schemes eliminate entirely: investment risk, longevity risk, and the risk of depleting the pot at an unsustainable rate.

The most damaging is often the least visible. A market fall shows up immediately in the pot’s value, investment risk is tangible. Longevity risk is slower to materialise, but outliving savings in a drawdown arrangement without an annuity floor is a genuine exposure for long-lived members.

Drawdown sustainability risk operates quietly in the background: withdrawing income at a rate the underlying investments cannot replenish compounds over years before the shortfall becomes apparent.

Why Unsustainable Drawdown Has Become the FCA’s Biggest DC Concern?

The rise in pension pot emptying has accelerated since Pension Freedoms gave DC holders unrestricted access from age 55. The Financial Conduct Authority has flagged unsustainable drawdown as a key consumer harm risk in the DC retirement market.

Members approaching retirement should request a pension forecast statement from their provider and review their intended withdrawal rate against a range of longevity scenarios before committing to an access strategy.

Sequence of returns risk is a specific DC pension danger distinct from general market volatility: poor investment returns in the two to three years immediately before or after retirement crystallise losses at the moment when the pension pot is largest, permanently reducing sustainable income even if long-term average returns later recover.

A defined benefit pension eliminates sequence of returns risk entirely, retirement income is fixed and independent of investment timing.

What the Pension Schemes Bill 2025 Means for DB and DC Members?

Three provisions within the Pension Schemes Bill 2025 carry direct consequences for pension holders on both sides of the DB and DC divide, and one of them is already shaping planning decisions made today.

DB surplus extraction is the first. Under provisions overseen by the Department for Work and Pensions, employers will be permitted to access surplus funds within defined benefit schemes under a revised framework, subject to member protection conditions.

The Pensions Regulator continues to monitor the funding implications for affected schemes.

The DC Inheritance Tax Change and What to Do Before April 2027

Unused DC pots will be brought within the Inheritance Tax estate from April 2027 under HMRC rules, a shift from the current position where DC savings sit entirely outside the estate. Those with substantial DC savings alongside other assets need to revisit their estate planning well before that date.

The UK pension inheritance tax changes carry a fixed effective date, and no retrospective relief is expected once the rules take effect.

The Pension Schemes Act 2021 formally enabled Collective Defined Contribution (CDC) schemes, a hybrid model sharing investment and longevity risk across the membership pool rather than placing it solely on the employer or the individual.

From April 2029, the National Insurance exemption on employer salary sacrifice pension contributions will be capped at £2,000 per year, affecting higher-earning DC members who use salary sacrifice to maximise pension funding.

Conclusion

For most private sector workers, a defined contribution pension is the only available option, the quality of the retirement it delivers depends entirely on the contribution decisions made during the working years.

For those with access to a defined benefit scheme, the guaranteed, inflation-linked income it provides is rarely worth surrendering.

Defined contribution vs defined benefit pension plan decisions mean the difference between guaranteed and investment-dependent retirement income for UK workers in 2025/26.

FAQ

What is an accrual rate in a defined benefit pension?

An accrual rate is the fraction of relevant salary added to a DB pension for each year of service. At 1/60th, a member earning £36,000 accrues £600 of annual pension per year. Common UK rates are 1/60th and 1/80th.

Can I have both a defined benefit and a defined contribution pension?

Yes. A DB workplace pension and a personal DC pension or SIPP can be held simultaneously. Combined contributions across both count toward the £60,000 annual allowance for 2025/26, exceeding this limit removes entitlement to full tax relief.

How do I find out whether I have a defined benefit or defined contribution pension?

Check the most recent pension statement, DB statements show a projected annual income; DC statements show a pot value. For untraceable pensions, the government’s Pension Tracing Service through MoneyHelper searches the national register free of charge.

What is a CARE pension and how does it differ from a final salary scheme?

A CARE pension calculates income from the average salary across the full membership period, with each year’s earnings revalued annually. A final salary scheme uses salary at or near retirement, typically producing a higher pension for long-serving members who retire at peak earnings.

What is the pension annual allowance for 2025/26?

The annual allowance for 2025/26 is £60,000, or 100% of annual earnings, whichever is lower. Contributions above this limit attract a tax charge. HMRC applies a tapered annual allowance for those with adjusted income exceeding £260,000.

Can I take a tax-free lump sum from a defined benefit pension?

Yes. DB members can commute part of their pension income for a tax-free lump sum, subject to the Lump Sum Allowance of £268,275. The scheme’s commutation factor determines how much annual income is surrendered per pound of lump sum taken.

What is the minimum pension access age in the UK?

The minimum pension access age is currently 55, rising to 57 from April 2028 under existing legislation. Members planning early retirement before 57 must account for this change, certain transitional protections may apply depending on individual scheme rules.

What protection does a defined contribution pension have if my provider fails?

DC savings held with FCA-authorised providers are covered by the FSCS up to £85,000 per provider. Members with pots above this threshold can reduce exposure by spreading savings across multiple separately authorised pension providers.

All figures in this article reflect published rates for the 2025/26 tax year and Pension Protection Fund compensation limits for 2024/25. For current annual allowance figures, compensation caps, and transfer rules, the primary sources are HMRC, the Pension Protection Fund‘s published schedule, and MoneyHelper.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or tax advice; always consult an FCA-authorised adviser before making pension decisions.