HMRC Notices For UK Pensioners Savings: Avoid The 2026 Trap

HMRC notices for UK pensioners savings are official tax communications, such as the PA302 Simple Assessment, issued when a retiree’s bank interest exceeds their Personal Savings Allowance.

In 2026, these letters act as a formal demand for unpaid tax that cannot be collected automatically via your tax code due to frozen thresholds.

The HMRC savings warning refers to the £3,000 threshold. In 2026, this is a vital collection boundary: if your tax debt from savings interest exceeds £3,000, HMRC cannot collect it via your pension tax code.

Instead, they will issue a formal PA302 Simple Assessment or force a transition into the Self-Assessment system.

The 2026 Pensioner Briefing: Avoiding the Savings Tax Trap

- New 2026/27 Rates: The Personal Allowance remains at £12,570, meaning many more pensioners will trigger tax bills this year as State Pension rates rise.

- PA302 Deadlines: Simple Assessment letters for the 2025/26 tax year begin arriving in June 2026.

- Automatic Reporting: UK banks must report all interest by 31 May 2026; HMRC’s Connect AI cross-references this with DWP records in real-time.

- Winter Fuel Payment Impact: Note that for the 2025/26 tax return, the Winter Fuel Payment is considered taxable income, which may inadvertently push your savings interest into a higher tax bracket.

What are HMRC Notices for UK Pensioners Savings?

HMRC notices for UK pensioners savings serve as the primary mechanism for the Revenue to recover tax on unearned income that has not been taxed at source.

Unlike salaried employees, most pensioners receive their State Pension and private pensions gross or via PAYE, which does not account for external interest.

According to HMRC guidelines, these notices are generated when the Connect AI system identifies a discrepancy between your reported income and the data provided by your financial institutions.

In 2026, the volume of these letters has increased by 40% as high interest rates continue to push basic-rate taxpayers over their £1,000 threshold.

Why UK Pensioners Are Receiving New Tax Bills?

If you have received an HMRC notice for the first time in your retirement, you are likely a victim of Fiscal Drag.

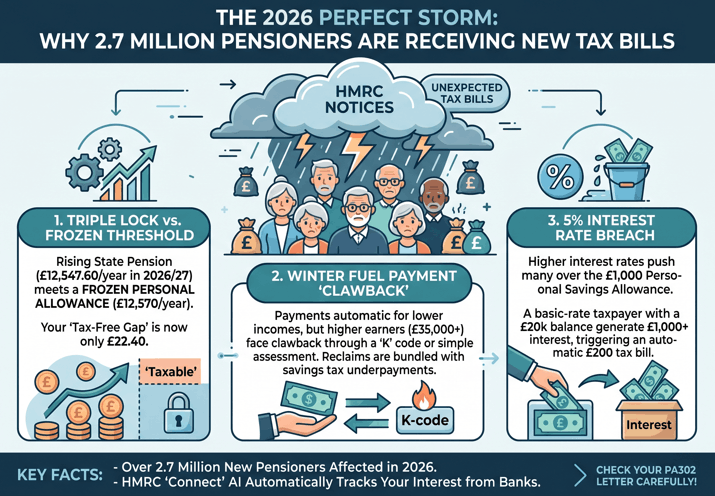

In 2026, three specific regulatory shifts have converged to pull a record 2.7 million pensioners into the tax net, many of whom have never owed tax on their savings before.

The Triple Lock vs. The Frozen Threshold

The primary driver is the collision between the rising State Pension and the frozen Personal Allowance (£12,570). Following the 4.8% increase in April 2026, the full New State Pension has reached £12,547.60 per year.

Because this is now just £22.40 away from the tax-free limit, almost any additional income, such as a small private pension or even modest bank interest, automatically triggers a tax liability. Effectively, your tax-free gap for savings has vanished.

The 2026 Winter Fuel Payment Clawback

A new factor for the 2025/26 and 2026/27 tax years is the revised Winter Fuel Payment eligibility. For pensioners earning over £35,000, HMRC is now automatically reclaiming these payments through the tax system.

If you are in this bracket, you will receive a notification of a tax code change (often a “K” code) or a Simple Assessment notice. This recovery is often bundled with savings tax underpayments, making the total figure on your HMRC notice look unexpectedly high.

The 5% Interest Rate Breach

In previous years, low interest rates meant you needed significant capital to exceed the £1,000 Personal Savings Allowance. In 2026, with many accounts still yielding 5%, a balance of just £20,000 generates £1,000 in interest.

Because your State Pension already uses up your Personal Allowance, this £1,000 is taxed at the basic rate (20%), leading to an automatic £200 tax bill that HMRC will notify you of via a PA302 letter.

Why did I get an HMRC notice now?

You are likely receiving an HMRC notice in 2026 because your State Pension has risen to £12,547.60, leaving only £22.40 of your tax-free allowance remaining. Any savings interest above this tiny margin is now taxable.

Due to the Connect AI system, HMRC receives real-time interest data from your bank and automatically issues a PA302 Simple Assessment if your tax code cannot be adjusted to collect the debt.

HMRC Savings Account Tax Letters: Why You Received a PA302?

If you have received an HMRC savings account tax letter, it is likely a PA302 Simple Assessment. This is issued because HMRC already has enough information about your income, from the DWP and your bank, to calculate your tax without requiring a formal tax return.

The letter will outline your total income for the tax year, including your State Pension, any private pensions, and the exact amount of savings interest reported by your bank.

It is critical to cross-reference these figures against your own year-end certificates (form R60), as banks occasionally report interest on joint accounts incorrectly, attributing 100% to one individual rather than a 50/50 split.

The HMRC Savings Warning: Does the £3,000 Limit Apply to You?

The widely discussed HMRC savings warning regarding £3,000 is one of the most misunderstood areas of UK tax policy. This figure does not represent a cap on your total savings, nor is it a threshold for being monitored.

In reality, the £3,000 limit is a collection boundary. If your tax bill on savings interest is under £3,000 and you have a PAYE pension, HMRC will typically code out the debt, deducting it from your monthly pension payments.

If the debt exceeds £3,000, HMRC cannot collect it this way and will issue a formal demand for payment or require you to register for Self-Assessment.

Understanding these triggers is essential, particularly as pension tax-free lump sum to be scrapped discussions may influence how retirees draw their income in the coming years.

Paying Tax on Savings When Retired: Calculating Your Allowances

Paying tax on savings when retired depends entirely on your total non-savings income. The hierarchy of tax-free allowances for 2026/27 is as follows:

- Personal Allowance: The first £12,570 of your total income is tax-free.

- Starting Rate for Savings: If your non-savings income (pension) is below £17,570, you get up to £5,000 of interest at a 0% rate.

- Personal Savings Allowance (PSA): Basic-rate taxpayers get an additional £1,000; higher-rate taxpayers get £500.

Fact-Check: The Truth Behind the £3,000 Savings Debt Warning

| Myth | Reality (2026) |

| I am limited to having £3,000 in my bank account. | FALSE. There is no limit on your savings balance. The £3,000 figure is the debt collection cap. If you owe HMRC more than £3,000 in tax, they cannot take it from your pension via a tax code and will demand a direct payment. |

| I must register for Self-Assessment if I earn any interest. | FALSE. Most pensioners are now under Simple Assessment. HMRC calculates your tax automatically using bank data. You only need to register if your savings income exceeds £10,000 or you have complex offshore assets. |

| The State Pension is tax-free, so I don’t owe anything. | FALSE. The State Pension is taxable income. Because the Personal Allowance is frozen at £12,570, the 2026 State Pension takes up nearly all your allowance, leaving very little space for tax-free savings interest. |

| HMRC doesn’t know about my small building society accounts. | FALSE. Under the Common Reporting Standard, every UK financial institution (including NS&I) is legally required to report your interest to HMRC by 31 May each year. |

| I only get a £1,000 Personal Savings Allowance. | FALSE (For many). If your pension income is low (under £17,570), you may also qualify for the £5,000 Starting Rate for Savings. This allows you to earn up to £6,000 in interest tax-free before paying a penny. |

| HMRC notices are always an accusation of tax evasion. | FALSE. Most nudge letters or PA302 notices are simply administrative adjustments due to fiscal drag, where frozen thresholds meet rising interest rates. |

HMRC Savings Notices for UK Pensioners: How Interest is Tracked

HMRC savings notices for UK pensioners are the result of the Automatic Exchange of Information (AEOI).

Every regulated UK financial institution, including National Savings & Investments (NS&I), submits a data file to HMRC containing your Name, Address, and total interest paid.

This data is processed by HMRC’s Connect system, which identifies individuals whose total income has crossed the threshold.

This transparency is why many are surprised by letters years after retirement. Managing your withdrawals is vital to staying below these triggers, especially given recent pension withdrawal rule changes UK which affect how you access your pots.

The Hidden £5,000 Starting Rate for Savings

A major blind spot in UK retirement planning is the Starting Rate for Savings. While many focus on the £1,000 PSA, the £5,000 Starting Rate is more valuable for low-income retirees.

If your total pension income is £13,000, you have used your £12,570 Personal Allowance and have £430 of taxable pension income.

Because this is less than £17,570, you qualify for the full £5,000 Starting Rate. This means you could earn up to £5,000 in interest + £1,000 PSA = £6,000 in savings interest before paying a penny in tax.

Stacking Allowances to Earn £18,570 Tax-Free

| Tax Allowance Type | 2026/27 Limit | Eligibility Criteria/Tax Rate |

| Personal Allowance | £12,570 | 0% Tax on all combined income (Pension + Savings). |

| Starting Rate for Savings | Up to £5,000 | 0% Tax on interest if your other income is below £17,570. |

| Personal Savings Allowance (PSA) | £1,000 | 0% Tax on interest for Basic Rate (20%) taxpayers. |

| Personal Savings Allowance (PSA) | £500 | 0% Tax on interest for Higher Rate (40%) taxpayers. |

| ISA Allowance | £20,000 | 100% Tax-free. Interest does not use up other allowances. |

| Additional Rate PSA | £0 (NIL) | No tax-free allowance if income exceeds £125,140. |

For the 2026/27 tax year, the Personal Allowance (£12,570) remains frozen despite the rising State Pension. This means that for the average pensioner, more of their private savings interest is now being pushed into the Taxable zone.

Pro Tip: To maximize your tax efficiency, you should apply your allowances in this specific order:

- Personal Allowance (Applied to your State Pension/Private Pension first).

- Starting Rate for Savings (Applied to the first £5,000 of interest if space remains).

- Personal Savings Allowance (The final £1,000 top-up for interest).

By stacking these, a pensioner with a low State Pension can technically earn up to £18,570 in total income before receiving an HMRC savings tax letter.

The Fiscal Drag Trigger

- Situation: Arthur, a retiree in 2026, receives the full New State Pension of £12,547.60 and has £15,000 in a 5% savings account.

- Root Cause: His pension leaves only £22.40 of his Personal Allowance. His £750 interest exceeds this, but because his total income is under £17,570, he qualifies for the Starting Rate for Savings.

- Solution: Arthur uses the GOV.UK portal to ensure HMRC applied his £5,000 Starting Rate.

- Takeaway: Always check if you qualify for the Starting Rate before paying a PA302 demand.

How do HMRC know if you have savings?

HMRC identifies your savings through Automatic Exchange of Information (AEOI) protocols. Under the Common Reporting Standard, banks provide annual reports including your National Insurance number and interest totals. HMRC then cross-references this against your DWP records.

If you receive a pension but have never worked, you may wonder about your status; however, I have never paid national insurance will i get a pension status does not exempt you from tax on any savings you do hold.

How much savings can a pensioner have in the bank before tax?

A pensioner can have any amount of savings; tax is only paid on the interest earned. At a 5% interest rate, a basic-rate taxpayer could have £20,000 in a standard savings account (earning £1,000 interest) before hitting their Personal Savings Allowance.

If they also qualify for the Starting Rate for Savings, that amount could rise significantly.

What is the HMRC warning for anyone with over £3,500 savings?

This specific warning relates to nudge letters sent to individuals whose interest data suggests they are nearing a higher tax bracket or have exceeded their PSA. It is often a precursor to a PA302 notice.

It is important to stay informed as UK state pension age retirement changes may alter your long-term income profile and tax liability.

Will I lose my State Pension if I have savings?

No. The State Pension is a non-means-tested benefit based on your National Insurance record. Having £1 million in savings will not reduce your State Pension. However, having significant savings will affect your eligibility for Pension Credit, which is means-tested.

How to Respond to an HMRC Savings Notice?

- Validate the ID: Ensure the letter is a genuine PA302 or P800.

- Gather Year-End Statements: Collect all R60 forms from your banks.

- Check for Gross vs Net: Most interest is paid gross; ensure HMRC hasn’t assumed tax was already deducted.

- Confirm Joint Account Splits: HMRC defaults to 50/50. If you own a different percentage, you must notify them.

- Use your Personal Tax Account: Login to the GOV.UK portal to see the data HMRC is using.

- Query within 60 Days: You must contact HMRC within this window to stop the debt collection process if the figures are wrong.

Self-Assessment vs. Simple Assessment: The 2026 Registration Myth

As of April 2026, HMRC’s system is a passive collection model. You do not need to register for a tax return simply because you earned interest.

- Simple Assessment (PA302): If you are a pensioner with untaxed interest under £10,000, HMRC will contact you. They use data from your bank and the DWP to issue a calculation.

- The £10,000 Trigger: You only need to register for Self-Assessment if your savings income exceeds £10,000.

- Proactive Warning: Do not register for Self-Assessment unless legally required; doing so can trigger failure to file penalties for a return you didn’t actually need.

How HMRC Automatically Audits Your Bank Interest?

HMRC identifies your interest via the Automatic Exchange of Information (AEOI), a global standard requiring UK banks to report your earnings by 31 May each year.

This data feeds directly into HMRC’s Connect AI system, which cross-references bank reports against your tax record in real-time. Even if you have never paid National Insurance, this automated surveillance tracks your interest and flags underpayments.

This high-tech transparency is why many retirees receive surprise tax notices years after stopping work; managing the scale of your withdrawals is now essential to maintaining a tax-efficient profile.

Conclusion

Receiving an HMRC notice is a result of the Revenue’s increasingly sophisticated digital surveillance of UK banking data.

For most retirees, these letters are not an accusation of wrongdoing but a corrective measure to account for interest earned above the frozen Personal Savings Allowance.

Receiving this correspondence requires diligent record-keeping to avoid overpaying on ghost interest figures reported by banks.

Ultimately, HMRC notices for UK pensioners savings means a mandatory tax reconciliation process for UK retirees in 2026.

FAQ

Do I need to notify HMRC of savings interest?

No. Banks report this automatically. However, if you are already in the Self-Assessment system for other reasons (e.g., rental income), you must include your savings interest on your return.

What happens if I don’t declare my savings?

If HMRC identifies undisclosed interest via their bank data-sharing network, they will issue a Discovery Assessment. This includes the tax owed plus interest and potential penalties for careless or deliberate non-disclosure.

Are ISAs included in HMRC savings notices?

No. Income from Individual Savings Accounts (ISAs) is legally exempt from income tax and does not count toward your Personal Savings Allowance or Starting Rate for Savings.

How much is the State Pension going up in 2026?

The State Pension is adjusted annually under the Triple Lock. For 2026, the increase is based on the highest of 2.5%, inflation, or average earnings growth. Check official GOV.UK announcements for the finalised weekly rates.

Can HMRC investigate my bank accounts?

Yes. Under Schedule 36 of the Finance Act 2008, HMRC has the power to issue Information Notices to banks to request specific transaction histories if they suspect tax evasion.

Is the income tax threshold rising for pensioners in 2026?

No. The Personal Allowance remains frozen at £12,570 until at least 2028. This fiscal drag is why more pensioners are receiving savings notices for the first time.

Do joint accounts affect my HMRC savings tax letter?

Yes. HMRC typically splits interest 50/50 between account holders. If one person is a non-taxpayer and the other is a higher-rate taxpayer, this split can significantly impact the total tax due.

What is a PA302 letter?

A PA302 is a Simple Assessment tax calculation. It is a legally binding demand for tax that HMRC issues when they believe they have all the data required to calculate your liability without a tax return.

What is the nudge letter deadline?

While nudge letters themselves often don’t have a statutory deadline, they usually suggest a 30-day window to check your records before HMRC proceeds with a formal assessment.