UK Cost Of Living Crisis 2026: DWP Payment Updates, New Energy Forecasts, And Budgeting Tips

The cost of living crisis is an ongoing economic period in the UK where the growth of essential household costs, primarily energy, food, and housing, outpaces the growth of real disposable income. In May 2026, while inflation has moderated to 3.3%, persistent high prices and rising interest rates continue to strain household resilience.

Navigating the 2026 financial landscape demands a clear view of how shifting fiscal policies intersect with DWP adjustments. This analysis details the current economic pressures alongside the latest updates to social security provisions.

Key Takeaways for 2026

- Inflation Status: CPI inflation stands at 3.3% (May 2026), driven by volatile global energy markets.

- Welfare Rebalancing: Universal Credit standard allowances rose by 6.2% in April 2026, though health-related elements were reduced for new claimants.

- Energy Forecast: After an April dip to £1,641, the Ofgem price cap is projected to rise to approximately £1,850 in July 2026.

- Wages vs. Prices: Real wage growth remains stagnant at 0.4%, leaving many households with less buffer for emergencies.

What is the UK Cost of Living Crisis?

The UK cost of living crisis is a multifaceted structural imbalance between household expenditure and income. While the initial shock was triggered by post-pandemic supply chain issues and the 2022 energy spike, the 2026 landscape is defined by entrenched price levels and restrictive borrowing costs.

Official ONS data confirms that the erosion of Real Household Disposable Income (RHDI) remains the central driver of this economic downturn.

Even as headline inflation figures fall, the cumulative effect of price increases since 2021 means that the cost of a standard weekly shop remains significantly higher than pre-crisis levels.

Current UK Cost of Living Statistics: The 2025–2026 Outlook

Market indicators from early 2026 suggest the economy is entering a period of precarious stabilization.

- CPI Inflation: 3.3% (as of March 2026).

- Food Inflation: Stabilised at 3.7%, but remains sensitive to global supply chain disruptions.

- Unemployment: Crept up to 4.9%, the highest since 2023.

- Interest Rates: The Bank of England base rate remains at 3.75%, impacting mortgage repayments for millions.

Key Fact: In 2026, the gap between nominal wage growth (3.6%) and CPI inflation (3.3%) has left the average UK worker with a real-term purchasing power increase of only 0.4%.

Purchasing power is the true metric of the crisis: although nominal wages rose by 3.6% in early 2026, once adjusted for the 3.3% inflation rate, the actual purchasing power of the average worker grew by only 0.4%.

When Will the Cost of Living Crisis End in the UK?

Economists at the Resolution Foundation suggest that ending the crisis is not a singular event but a gradual recovery of living standards. Current projections indicate that typical household incomes will not return to 2021 levels until 2028 or 2029.

For most families, the crisis will end only when wage growth consistently outstrips inflation for a sustained three-year period.

This long-term outlook is particularly concerning for those nearing the end of their careers, especially given recent UK state pension age retirement changes that may force many to stay in the workforce longer than planned.

The Bank of England aims to bring inflation back to a 2% target by 2027. However, the 2026 economic outlook remains low-growth, with GDP expected to expand by only 0.6%.

Meaningful recovery remains tethered to the real wage gap; until earnings growth reliably outpaces the cost of essentials for several consecutive years, the financial pressure on the average household will persist.

The Pay Rise Trap and the Cost of Living Crisis

A common misconception is that falling inflation means prices are coming down. In reality, falling inflation simply means prices are rising more slowly.

Fiscal Drag occurs because the government has frozen personal tax thresholds. As your wages increase to keep up with inflation, you are pushed into higher tax brackets, or more of your income is taxed at the basic rate.

You may earn more on paper, but your net take-home pay buys fewer goods than it did a year ago. To combat this, you must review your pension contributions or tax-efficient savings (ISAs) to mitigate the impact of bracket creep.

However, many find the current system for older demographics problematic, often citing the new state pension being unfair to existing pensioners who do not benefit from the same uplift structures as those reaching retirement age today.

Is a UK Recession Coming in 2026?

The probability of a technical recession (two consecutive quarters of negative growth) remains at approximately 45% for 2026. While consumer spending has proven more resilient than expected, the delayed impact of high interest rates is now fully hitting homeowners on fixed-rate deals.

If energy prices spike again in Q3 2026 as forecast, the UK could see a shallow recession. However, most analysts predict a stagnation period, zero or near-zero growth, rather than a deep economic crash.

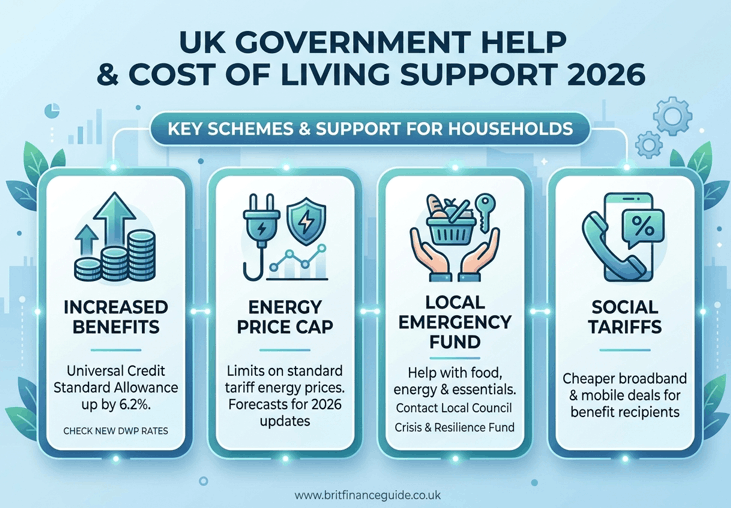

Government Help and Cost of Living Crisis Support 2026

Direct, flat-rate Cost of Living Payments (like the £900 issued in 2023/24) have been phased out for 2026. The government has transitioned to a model of Targeted Uprating. Instead of one-off cash injections, the DWP has permanently increased the Universal Credit Standard Allowance by more than the rate of inflation (6.2%) as of April 2026.

For immediate emergencies, you can still access the Crisis and Resilience Fund (which replaced the Household Support Fund). This is administered by local councils and can provide help with food, energy bills, and essential white goods.

Who Suffers the Most from the Cost of Living Crisis?

Data consistently shows that the crisis disproportionately affects households with the lowest 20% of income. These families spend a larger proportion of their budget on inelastic goods, items like heating and bread that cannot be easily cut back.

Additionally, Unsung Britain, the cohort of low-to-middle income workers who do not qualify for most means-tested benefits, is increasingly reliant on credit to cover basic monthly shortfalls.

Single-parent households and those with long-term disabilities also face higher-than-average inflationary pressure.

Older residents on fixed incomes are similarly at risk, as their financial planning is frequently disrupted by the UK state pension age increase, which shifts the goalposts for those relying on state support. These overlapping pressures create an inescapable financial bottleneck for those with limited workforce mobility.

UK Economy Facts and Cost of Living Crisis Myths

| Myth | Reality |

| Falling inflation means prices are getting cheaper. | Prices are still rising, just at a slower pace. Deflation is rare. |

| The 2026 Payment Freeze means no help is available. | Direct payments ended, but UC standard rates were boosted by 6.2%. |

| High interest rates only hurt people with mortgages. | Rates affect renters too, as landlords pass on increased financing costs. |

| The energy crisis is completely over since April 2026. | The cap fell to £1,641 but is forecast to hit £1,850 by July. |

| Increasing the minimum wage is the primary cause of inflation. | Global energy and supply chain shocks remain the dominant drivers. |

Will Universal Credit Increase in 2026?

Yes, Universal Credit rates increased on 6 April 2026. The standard allowance rose by 6.2%, which was intentionally set above the inflation rate to help families catch up from previous years.

However, if you are a new claimant with a health condition, be aware that the Limited Capability for Work and Work-Related Activity (LCWRA) element has been reduced to £217.26 per month for most new cases.

You should check your online journal to see exactly when the new rates apply to your specific assessment period.

New 2026 DWP Universal Credit Payment Rates

The 2026/27 financial year introduces a significant adjustment to the social security safety net. These updated DWP figures provide the exact breakdown of the 6.2% standard allowance increase required to calculate your household’s monthly disposable income.

| Circumstance | Monthly Rate (Pre-April 2026) | Monthly Rate (From April 2026) |

| Single, aged 25 or over | £400.14 | £424.90 |

| Single, under 25 | £316.98 | £338.58 |

| Joint claimants (one/both 25+) | £628.10 | £666.97 |

| LCWRA Element (New Claimants)* | £423.27 | £217.26 |

*Note: Under the 2025 Act, the LCWRA rate for new claimants has been significantly reduced to rebalance the benefit, though existing claimants are protected.

How to Access Financial Support Today?

The following checklist provides a framework for securing all available statutory support and emergency funding.

- Verify Full Statutory Entitlement: Use an independent calculator (e.g., Turn2us) to ensure you are claiming your full entitlement, including the 2026 boosted UC rates.

- Contact Your Local Council: Ask about the Crisis and Resilience Fund. You do not always need to be on benefits to qualify for emergency help.

- Check for Social Tariffs: If you receive UC, you are likely eligible for significantly cheaper broadband and mobile deals, which can save £200+ per year.

- Review Energy Direct Debits: Since the cap changed in April and will change again in July, ensure your supplier has not set your monthly payments unnecessarily high.

- Apply for a Budgeting Advance: If you have been on UC for 6 months, you can apply for an interest-free loan for one-off costs via your online journal.

Conclusion

Managing the cost of living in 2026 requires a proactive approach to welfare eligibility and an awareness of upcoming fiscal drag effects.

While the headline inflation rate of 3.3% suggests a cooling economy, the reality for many UK households is a continued struggle against high base prices and rising energy costs forecast for late 2026.

By utilizing the 6.2% increase in Universal Credit standard allowances and accessing local Crisis and Resilience funding, vulnerable households can secure essential support.

Ultimately, the cost of living crisis means a sustained gap between earnings and essentials for UK households throughout 2026.

Frequently Asked Questions

Is a UK recession coming in 2026?

Current economic indicators suggest a 45% chance of a technical recession in 2026. While the economy grew by a modest 0.1% in the last quarter, the impact of high interest rates on household consumption remains a significant downside risk.

Is there a cost of living payment in 2026?

No, there are no scheduled nationwide cost of living payments for the 2026/27 tax year. The DWP has instead moved to increasing the standard monthly Universal Credit payments and funding local authority Crisis and Resilience schemes.

Will the energy price cap go up in July 2026?

Yes. Industry analysts, including Cornwall Insight, predict the Ofgem price cap will rise from its current £1,641 to approximately £1,850 in July. This is due to increased wholesale gas prices following geopolitical tensions in the Middle East.

Can you live on £1000 a month in the UK?

Living on £1,000 a month is extremely challenging in 2026, especially for those in the private rental sector. Outside of London, average rents and essential utilities often exceed £850, leaving very little for food or transport.

Who is eligible for the Crisis and Resilience Fund?

Eligibility is determined by your local council. Generally, it is aimed at those facing immediate hardship (e.g., being unable to afford a meal or heat their home). You are usually required to show proof of low income or a sudden financial shock.

What is the new Universal Credit rate for 2026?

For a single person over 25, the standard allowance is now £424.90 per month. For a couple where at least one person is over 25, the rate is £666.97. These rates represent a 6.2% increase from the previous year.

Is inflation still a problem in 2026?

Yes. While the 3.3% rate is lower than the 11% peaks of 2022, it is still above the Bank of England‘s 2% target. More importantly, the cumulative inflation of the last four years means the cost of living remains historically high.

Do I need to apply for the benefit increase?

No. If you are already receiving DWP benefits like Universal Credit, PIP, or the State Pension, the 2026 increases will be applied automatically to your payments.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute professional financial or legal advice; readers should consult a qualified advisor or official government resources before making financial decisions.