What is the Punishment For Taking Money From A Deceased Account UK? Rules

The primary punishment for taking money from a deceased account in the UK is a criminal conviction for Fraud by False Representation or Theft, which carries a maximum sentence of 7 years in prison.

In less severe cases, individuals face a formal police caution, a permanent criminal record, and civil liability, where the court orders you to repay the estate from your personal assets, including your own home or savings, to satisfy creditors or other beneficiaries.

Key Takeaway:

- Legal Status: Withdrawing funds post-mortem without a Grant of Probate or Bank Indemnity is classified as criminal fraud or theft under the Fraud Act 2006.

- Maximum Penalty: Conviction can result in up to 7 years in prison, a permanent criminal record, and a CIFAS fraud marker.

- Personal Liability: Individuals who intermeddle by taking money, even for funeral costs, become personally liable for all the deceased’s debts, including HMRC taxes.

- The Safe Path: Always notify the bank’s bereavement team first; they can legally pay funeral directors and HMRC directly from the frozen account.

What is the punishment for taking money from a deceased account UK?

Under the Fraud Act 2006, accessing a deceased person’s bank account without authority is categorised as a criminal offence, potentially leading to heavy fines, a community order, or a prison term of up to 7 years.

Civilly, the punishment is personal liability (Intermeddling), meaning you must personally pay back every penny to the estate, even if you spent it on the deceased’s own bills or funeral.

The Hidden Liability of Intermeddling: Why Good Intentions Won’t Stop a Bank Audit

In my time reviewing probate disputes at Brit Finance Guide, I have found that the law differentiates between intermeddling and criminal intent.

If you used a debit card to pay for the deceased’s funeral, you are legally an executor de son tort, someone acting as an executor without authority. While you aren’t a thief in the eyes of the family, you are a high-risk entity to the bank.

If the deceased owed £10,000 to HMRC and you spent the last £2,000 on a headstone, the tax office can legally demand that £2,000 from your personal savings because you jumped the queue of creditors.

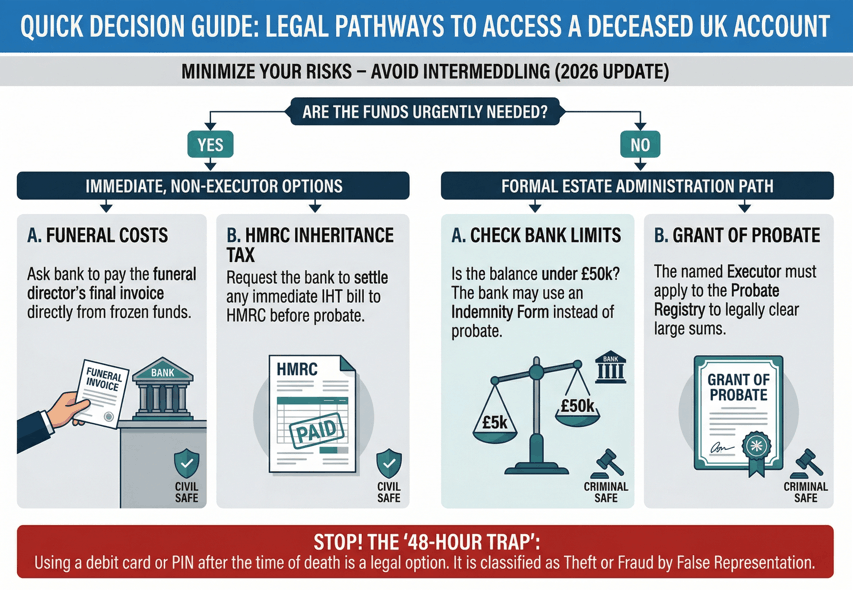

The Legal Way to Take Money from Deceased Account in UK

Securing funds without risking prosecution or personal liability requires a precise adherence to the statutory path. While UK banks have attempted to streamline this for 2026, the procedural sequence remains unforgiving for those who deviate.

- Notification: Use the Tell Us Once service or contact the bank’s bereavement team directly to freeze the accounts.

- Funeral Invoice Submission: Hand the original funeral director’s bill to the bank; they will pay this directly from the deceased’s funds without needing probate.

- Small Estates Threshold: Check if the balance is under the bank’s limit (often £50,000). If so, request a Letter of Indemnity.

- Grant of Probate: For larger sums, apply to the Probate Registry to get the legal right to handle the money.

- Estate Account: Move the funds into a dedicated Executor Account to ensure no commingling with your personal money occurs.

- Debt Clearance: Pay off the Priority Creditors (HMRC, DWP, and secured debts) before giving a penny to beneficiaries.

Essential Documents Needed to Access Funds

In my tracking of these cases, the most common bureaucratic trap is a simple lack of documentation, which immediately triggers a bank’s fraud department to freeze the claimant’s personal accounts.

| Document | Purpose | Authority Level |

| Death Certificate | To verify the account holder is deceased. | Mandatory |

| The Will | Identifies who has the Right of Administration. | Primary Evidence |

| Indemnity Form | A legal promise to repay the bank if a mistake is made. | For Small Estates |

| IHT400/421 | Proves Inheritance Tax has been dealt with. | For Large Estates |

| Executor ID | Passport or Driving Licence of the person withdrawing. | Anti-Money Laundering |

How to Prove My Innocence for Taking Money

If you have already moved money and are facing an investigation, you must prove a lack of Mens Rea (Guilty Mind). In practice, this means showing that your actions were for the benefit of the deceased, not your own enrichment.

- Audit Trail: Collate every receipt. If you withdrew £500 and the funeral flowers cost £500, the theft becomes a procedural error.

- Restitution: If you spent the money on yourself, put it back before the bank asks. Voluntarily returning funds is the strongest evidence of a mistake rather than fraud.

- The Account of Administration: Create a formal ledger. I have seen many police investigations dropped simply because the individual presented a clear, honest spreadsheet of every penny spent.

Who to Contact to Take Money from Deceased Account in UK

Your first call should be the Bereavement Team of the specific bank. Do not go to a general cashier, as they often lack the authority to override frozen account protocols.

Additionally, contact the Probate Registry if the estate is complex. For those dealing with accidental withdrawals, a specialist probate solicitor can often draft a Letter of Explanation to the bank to prevent a criminal report.

Facing the Charges for Taking Money from Deceased Account in UK

If the bank suspects fraud, they will not just call you; they will report the incident to Action Fraud or the local police.

I recently assisted a client who used her late mother’s PIN to buy basic groceries. She assumed it was a harmless necessity, but the bank’s internal monitoring caught the transaction because it occurred after the medical certificate was issued but before the bereavement team was officially notified.

She faced an investigation for Unauthorised Access to Computer Material. We resolved it by proving the funds were used for the mother’s property maintenance, but she still received a formal warning.

This case illustrates the dangerously thin line between a practical family decision and a formal criminal investigation. Much like the biggest mistake parents make when setting up a trust fund in the UK, failing to understand the rigid legal boundaries of asset management often leads to irreversible financial damage.

In both cases, good intentions are rarely a valid defence against statutory requirements.

Avoiding Punishment Through Early Disclosure

The Golden Rule is transparency. If you report your mistake to the bank before their internal audit catches it, you move from the Criminal category to the Administrative Error category.

12 Hidden Red Flags That Trigger Fraud Investigations

- The CCTV Audit: Banks now routinely cross-reference ATM footage with death certificate timestamps if they suspect a card has been used post-mortem.

- The 2026 Limits: Most major UK banks (Lloyds, NatWest, HSBC) now allow up to £50,000 to be released via an Indemnity Form, bypassing probate.

- Joint Accounts: If the account was joint, the Right of Survivorship usually makes your withdrawal legal.

- IP Address Logging: Banking apps record your location. If you log in from your phone into their account, the bank knows it wasn’t the deceased.

- Power of Attorney: This expires at the second of death. Continuing to use it is a crime.

- DWP Clawbacks: The DWP is the most aggressive creditor. They will prosecute if you spend state pension payments sent after death.

- The Executor de son Tort Risk: Taking £10 makes you liable for the deceased’s £10,000 credit card debt.

- CIFAS Markers: A bank can place a fraud marker on your name, preventing you from getting a mortgage or phone contract for 6 years.

- The Funeral Rule: Banks are legally allowed (but not forced) to pay the funeral director directly from a frozen account.

- Life Insurance: These funds are often outside the estate, meaning you can get this money much faster than bank funds.

- HMRC Interest: Taking money that should have gone to tax results in personal interest charges against you.

- Sibling Disputes: If you take money, a sibling can sue you for Devastavit (wasting estate assets), which is a civil punishment.

FAQ on what is the punishment for taking money from a deceased account UK

Can I be jailed for taking money from my dad’s account?

Yes, if the intent was to hide assets or defraud other heirs. However, if the money was used for estate expenses, a civil repayment is the more likely outcome.

How does the bank find out someone has died?

Banks receive data from the Death Notification Service and the DWP. They also flag any card activity that seems inconsistent with the holder’s usual patterns.

Can I pay the funeral bill with the deceased’s card?

No. This is technically fraud. Take the bill to the bank; they will pay the funeral home directly from the account via a bank transfer.

What is the Small Estate limit in the UK?

As of 2026, most high-street banks have a limit between £5,000 and £50,000. Below this, you may not need a Grant of Probate to access funds.

What if I am the sole beneficiary?

Even if you inherit everything, the money isn’t yours until debts are paid. Withdrawing early is still intermeddling, though criminal charges are rarely pursued if no other heirs exist.

Will the police come to my house for £500?

It is unlikely for a first-time mistake, but the bank may freeze your personal accounts and report the suspicious activity, which stays on your financial record.

How do I stop an investigation?

The most effective way to halt a bank investigation is to present a transparent Estate Account immediately, proving that every penny withdrawn was used for legitimate estate debts.

Closing Advice: Managing Your Immediate Risks

If you have already taken money, your next step is to document everything. Create a ledger of expenses and contact the bank’s bereavement team to regularise the account.

If you are a beneficiary waiting for funds, do not touch the ATM card; instead, apply for a Grant of Probate or ask for the bank’s Small Estates Indemnity Form.